Trusted by Insurance Leaders

Powering Smarter, Faster Insurance Operations

Embedding intelligence across insurance workflows to improve speed, accuracy, and operational efficiency

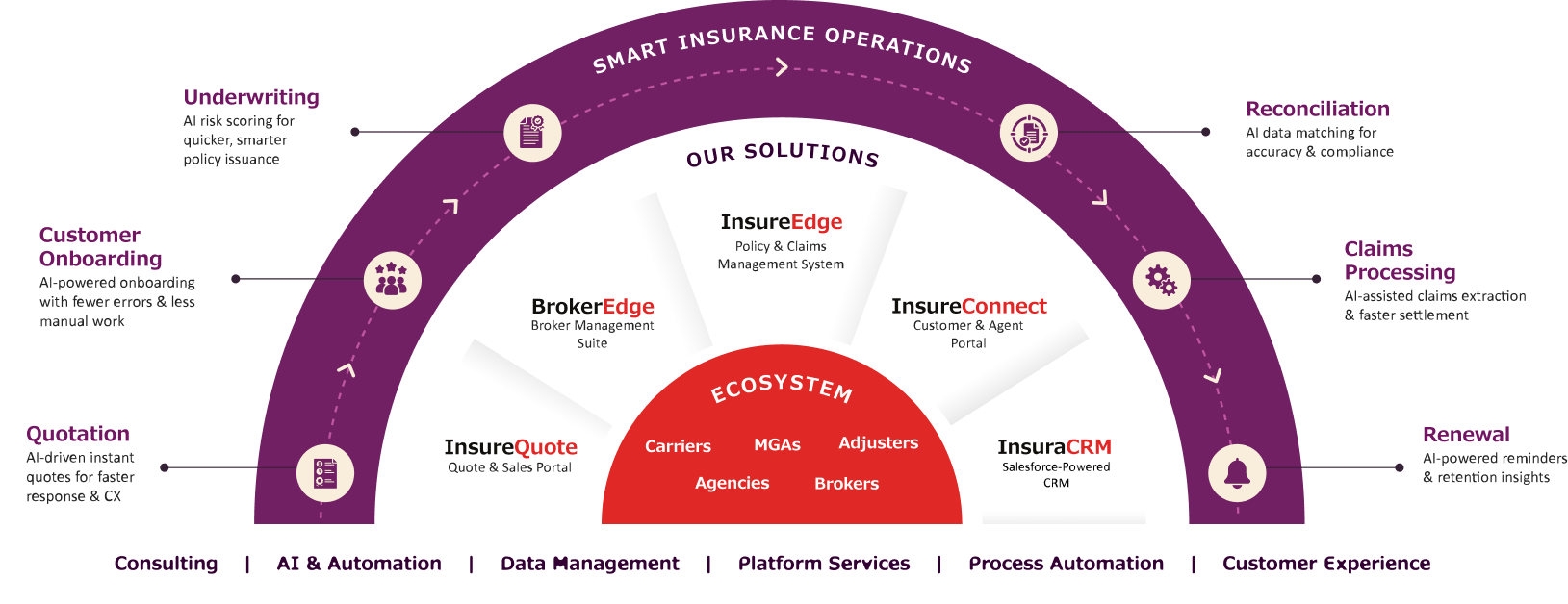

Business demands greater operational effectiveness as digital-savvy insurance customers expect fast, simple, and seamless experiences, without compromising regulatory compliance or operational control. Yet legacy systems and fragmented workflows continue to slow product launches, limit scalability, and create inconsistencies across underwriting, policy, and claims.

Damco helps insurers move from manual, rules-heavy operations to AI-enabled execution. By embedding intelligence across workflows, data extraction, decision support, triage, and automation, we help insurers reduce friction, improve accuracy, and scale operations with confidence. Backed by deep insurance domain expertise and proven delivery capabilities, Damco designs and implements AI-driven solutions that free insurance teams to focus on higher-value work.

30+

Years of experience delivering technology solutions across the insurance ecosystem

900+

Engagements across implementations and large-scale insurance projects

32+

Countries with active project execution and delivery presence across the USA, UK, Luxembourg, Middle East, Australia, and India

98.8%

Client satisfaction and long-term retention rate

Analyst Recognition & Awards

Recognized by Leading Industry Analysts and Partners

Featured as one of the major contenders in the Insurance Platforms IT Services PEAK Matrix® Assessment, 2022

Highlighted as one of the key aspirants in Application and Digital Services in L&A Insurance – Service Provider, 2021

Featured as a key insurance technology company in the Global Health Policy Administration System Report, 2021

Recognized as a premier insurtech company in Everest’s L&A ADS Providers Peak Matrix®, 2020

Highlighted as a leading insurance technology company in the Policy Administration Systems: P&C Insurance, Latin America Edition, 2021

Celebrating Customer Wins

Real-world outcomes delivered for carriers, brokers, MGAs, and adjusters, focused on speed, accuracy, and operational scale.

A Caribbean Insurer Eliminated Operational Bottlenecks with InsureEdge

Unified policy, billing, and claims processes into one automated system to accelerate operations and improve customer service.

A U.S. Life Insurance Provider Saves $2 Million and Improves Revenue Through Unified CX Platform

Integrated customer-facing processes on a modern digital platform to simplify policyholder interactions, reduce licensing and maintenance costs, and improve operational efficiency.

A Leading UAE-Based Insurer Accelerated Policy & Claims with InsureEdge

Digitized policy and claims workflows to achieve 70% faster issuance and significantly fewer reconciliation errors.

Technology Partners

Latest Insights

Expert insights on insurance operations, technology, and execution.

AI Readiness Checklist for Insurance

Explains how to bridge the gap between AI investment and AI success and how to strengthen organizational readiness for AI.

Fighting Insurance Fraud with AI

Illustrates how AI identifies frauds early, reduces false positives, and helps insurers detect and prevent frauds fast.

Top Innovative Technology Solutions for the Modern-Day Insurance Broker

Explains how digital platforms empower brokers to deliver faster quotes, manage submissions effectively, and strengthen client relationships through automation and smart workflows.