Why do insurance companies lose money on claims that should be profitable? Because inefficient claims management wastes resources on every claim processed. Manual processes, duplicate work, and delayed settlements all drain profit margins silently. That silent erosion of margin rarely stems from isolated failures; it is structural.

Fixing a structural problem requires more than incremental process fixes. Claims management software eliminates these profit leaks by automating workflows, detecting fraud early, and processing claims faster with fewer resources required. The following breakdown explores the hidden costs of inefficient claims management, examines why traditional operations bleed value, highlights the architectural advantages of claims management solution, and explains how to realize the ROI of insurance claims management system.

What Are the Hidden Costs of Inefficient Claims Management?

Inefficient claims management quietly erodes insurer profitability, decision quality, and resilience long before losses appear on financial statements, creating structural drag that compounds across margins, talent, compliance, and enterprise agility.

1. Margin Erosion Happens Long Before the Claim Is Paid

Margin loss in claims rarely begins at settlement. It starts upstream during intake, triage, and early assessment, where delays, poor segmentation, and manual handoffs increase claim severity before financial controls are even applied. By the time a claim is paid, much of the margin impact is already locked in.

This is a structural issue, not an operational one. Inefficient early decisions inflate indemnity costs, recovery leakage, and legal exposure in ways that pricing and underwriting cannot later correct. Claims inefficiency quietly converts controllable costs into deterministic losses.

2. Claims Inefficiency Distorts Financial Truth

Inefficient claims management weakens the accuracy of reserves, loss projections, and period-end reporting. When claims linger unresolved, finance teams work with incomplete signals, which can overstate stability or hide emerging deterioration in claims severity.

That distortion creates a false sense of control at the leadership level. Strategic decisions around pricing, capital allocation, and expense management become less reliable because the claims function is no longer reflecting the true cost of risk in real time.

3. Talent Is Consumed by Low-Value Work

Highly skilled claims professionals are increasingly absorbed by administrative rework, such as chasing documentation, reconciling inconsistencies, and managing avoidable exceptions created by inefficient systems. This misallocation of expertise reduces both morale and productivity across claims organizations.

At an enterprise level, this represents opportunity cost. When senior adjusters and claims leaders are buried in executional friction, they are unavailable for severity control, fraud detection, or portfolio insight generation; the core activities that protect margins and inform strategy.

4. Operational Drag Limits Strategic Agility

Claims inefficiency slows the entire operating model because every unresolved case creates backlog, escalations, and cross-functional dependency. Leaders lose the ability to respond quickly to market shifts, large loss events, or changing customer expectations because the process is already congested.

That operational drag is especially costly in environments where speed matters to competitiveness. When claims teams are overloaded by avoidable work, the enterprise cannot easily scale service or redirect capacity toward transformation initiatives.

5. Regulatory Non-Compliance Penalties

Poor claims management increases exposure to missed deadlines, incomplete documentation, and inconsistent handling standards. In regulated environments, these failures can trigger penalties, audits, remediation costs, and reputational damage that far exceed the original processing expense.

Beyond fines or remediation costs, the bigger issue is that compliance risk compounds when controls are weak, and exceptions are normalized. A claims operation that cannot prove consistency becomes a liability because it invites scrutiny from regulators and litigants alike.

Why Are Traditional Claims Operations Bleeding Value?

Traditional claims operations were built for predictability and volume efficiency, not today’s volatility, regulatory scrutiny, and margin pressure. As a result, they structurally leak value across cost, speed, insight, and strategic alignment.

I. Claims Processes Designed for Stability, Not Volatility

Traditional claims operating models were engineered for predictable claim volumes, familiar loss types, linear handoffs, and standardized decisions. That works until catastrophic events, litigation spikes, fraud patterns, or severity inflation introduce volatility that the process cannot absorb without backlogs and inconsistency.

This mismatch creates asymmetric downside risk. When workflows are optimized for routine cases, every exception becomes a manual intervention, and operational resilience drops exactly when the business needs speed, judgment, and capacity the most.

II. Cost Leakage Is Embedded in the Operating Model

In legacy claims environments, leakage is not an exception; it is structurally embedded. Overpayments, missed recoveries, unnecessary escalations, settlement delays, and inconsistent reserving practices quietly increase cost across the lifecycle. EY’s 2025 P&C Claims Transformation analysis found that claims leakage represents approximately 7%-14% of total carrier spending, underscoring how deeply inefficiency is rooted into traditional operating models.

This embedded leakage compounds silently. From a leadership perspective, this means the organization is paying for inefficiency multiple times. Each manual handoff, rework cycle, and delayed subrogation opportunity chips away at margin without appearing as a single, visible expense line.

III. Decision-Making Is Slow Where Speed Creates Value

Traditional claims operations rely heavily on manual escalation paths and sequential approvals. Decisions that should be instantaneous are delayed by process inertia, increasing claim duration, customer dissatisfaction, and ultimate cost.

Speed creates value because it reduces indemnity growth, lowers expense per claim, and improves closure rates. When decisions are delayed, the organization loses leverage with vendors, claimants, and internal stakeholders at the exact point where timing matters most.

IV. Claims Data Lives in Retrospective Silos

Legacy systems treat claims data as a historical record, not a real-time decision asset. Information is captured for reporting and compliance, then analyzed weeks or months later, long after its value for influencing outcomes has passed.

This retrospective orientation deprives the enterprise of actionable intelligence. Claims insights fail to inform underwriting, pricing, or risk strategy when they matter most. The organization learns from claims only after the financial impact is irreversibly realized.

V. Operating Expense Grows Faster than Premium Growth

As claims complexity increases, traditional operations respond by adding people, not intelligence. Headcount scales linearly while productivity plateaus, pushing expense ratios upward. The NAIC’s 2025 Mid-Year Insurance Industry Analysis shows that claims adjustment and administrative expenses rose 6.2% year over year, outpacing premium growth and directly compressing profit margins.

For senior leadership, this creates a structural imbalance. Premium growth cannot sustainably absorb rising claims operating costs. If claims expense rises faster than top-line growth, the business is effectively buying complexity with margin, leaving less room for investment in customer experience, analytics, automation, and loss prevention.

VI. Expertise Is Applied Too Late in the Lifecycle

In traditional models, experienced adjusters and specialists are engaged after claims have already escalated. By then, the value has already leaked.

High-value expertise delivers the greatest impact when applied early, during triage and severity forecasting. Late intervention may control damage, but it cannot restore missed opportunities for early resolution, recovery optimization, or behavioral steering.

VII. Claims Functions Remain Disconnected from Enterprise Strategy

Claims are often treated as a back-office function instead of a strategic source of risk intelligence, customer insight, and cost discipline. As a result, claims priorities may not align with underwriting, distribution, finance, or enterprise transformation initiatives.

That disconnect limits enterprise value creation. When claims data and operating metrics are not tied to strategic goals, leaders miss opportunities to reduce loss, improve retention, strengthen pricing, and turn claims from a cost center into a performance lever.

Embrace Insurance Claims Modernization with Advanced Claims Management System

What Are the Architectural Advantages of Claims Management Software?

Modern claims management software is no longer a workflow upgrade; it is an architectural recalibration of how insurers absorb volume, manage cost, protect data, and generate insight. Purpose-built claims platforms are designed to scale, integrate, and adapt under real-world volatility. These architectural advantages determine whether claims operations become a margin stabilizer or a structural liability as complexity and customer expectations accelerate.

1. Scalable Cloud-Based Architecture for High-Volume Claims

Cloud-native claims platforms elastically scale processing capacity during demand spikes without proportional infrastructure or staffing cost increases. This elasticity prevents service degradation exactly when resiliency matters most.

For leadership, scalability is a financial control lever. It converts fixed infrastructure cost into variable operating expense, protecting margins during volatility while avoiding overinvestment during steady-state periods.

2. Modular Design Enabling Seamless Customization and Integration

Modular claims architectures separate core transaction processing from business rules, workflows, and integrations. This allows insurers to customize processes, add capabilities, or integrate platforms without destabilizing the entire system.

Strategically, modularity preserves agility. It enables targeted enhancements without lengthy rebuild cycles that slow time-to-value and consume IT capacity.

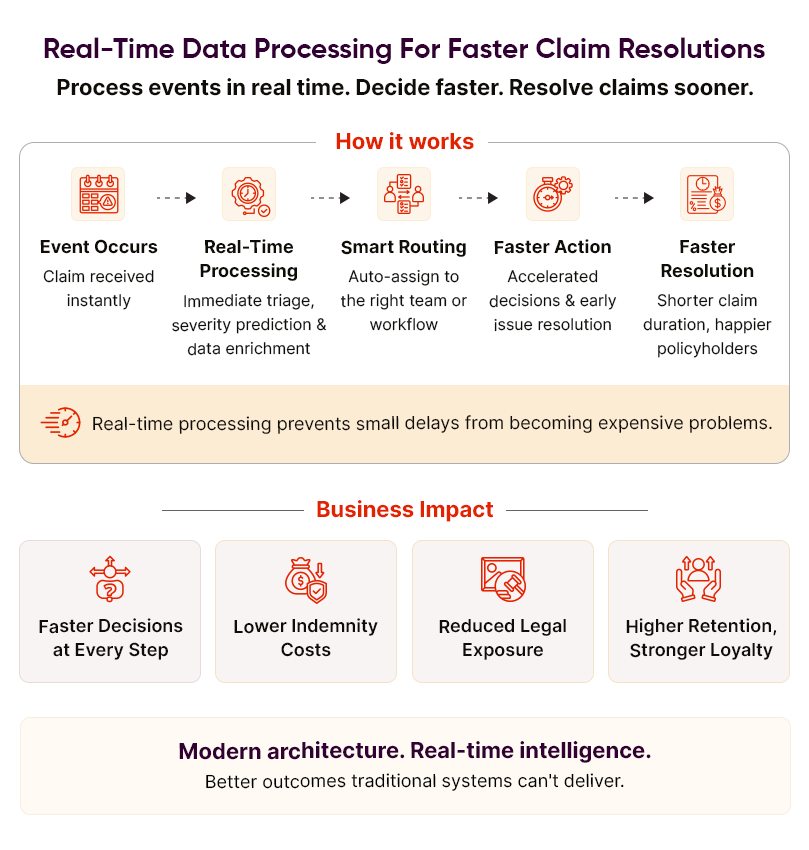

3. Real-Time Data Processing for Faster Claim Resolutions

Modern claims platforms process events in real time rather than batch cycles, enabling immediate triage, severity prediction, and routing decisions. This reduces claim duration and prevents early inefficiencies from compounding downstream.

For insurers, real-time processing directly links architecture to outcome. Faster decisions reduce indemnity cost, legal exposure, and customer churn; benefits that traditional systems structurally cannot deliver.

4. Robust Security Frameworks Protecting Sensitive Policyholder Data

Claims platforms handle personal, financial, medical, and legal information that must be protected at every stage. Strong security architecture typically includes role-based access, encryption, audit trails, and controlled data retention to reduce exposure and preserve trust.

At the executive level, this is not just an IT safeguard; it is a risk-management requirement. A secure claims architecture reduces breach likelihood, supports regulatory expectations, and protects the organization from legal, financial, and reputational damage.

5. Advanced Analytics Dashboards Driving Cost-Saving Insights

Analytics dashboards turn claims data into operational intelligence by exposing severity trends, leakage patterns, and adjuster performance in one view. This visibility helps leadership identify where cost is rising and where intervention will matter most.

The strategic advantage is decision quality. Instead of relying on periodic reports, executives can act on current performance signals, prioritize loss-control actions, and align claims management with finance, underwriting, and enterprise profitability goals.

6. API-First Approach for Ecosystem-Wide Connectivity

An API-first architecture makes claims software easier to connect with policy administration, billing, document management, fraud tools, repair networks, and CRM systems. Architecturally, this eliminates the fragmentation that often slows claims resolution and creates duplicate data entry.

For insurers, connectivity is a force multiplier. It enables smoother partner collaboration, faster data exchange, and a more coordinated customer journey, while also reducing integration costs every time the ecosystem expands or changes.

“The claims journey of the future will be increasingly automated, digital and data-driven,”

– Lisa Bartlett, Managing Director at Gallagher.

7. Low-Code Configuration Minimizing IT Dependency

Low-code configuration allows business teams to modify forms, rules, workflows, and notifications without depending on long IT release cycles. That is especially valuable in claims, where regulatory changes and operational adjustments often cannot wait for major development work.

The executive benefit is organizational agility. Claims leaders can respond faster to market, product, or compliance changes while IT focuses on higher-value architecture and governance work.

How to Realize the ROI of Insurance Claims Management Software?

Investing in a modern insurance claims management software is a strategic decision that yields significant benefits for businesses. Insurers need to plan well to get the maximum return on investment (ROI). Explore some key strategies to help insurers maximize the ROI from their insurance claim management software:

I. Identify the Processes for Optimization

Map the business processes to identify bottlenecks and areas for improvement. It helps in weeding out inefficiencies, delays, and pain points. Thereafter, harness the automation capabilities of the claims management solutions and streamline the processes. For instance, the software can be used to automate data-entry tasks. By automating and optimizing processes, insurers improve efficiency while reducing the risk of human errors.

What Is the Role of Insurance Management Systems in Streamlining Claims Processing?

II. Optimize Fraud Detection Capability

Implement artificial intelligence/machine learning (AI/ML) algorithms and analytics within the software for insurance claims fraud detection. With this proactive approach, insurers reduce fraudulent payouts and improve underwriting accuracy. As such, insurers must choose software that allows them to define and customize rules and parameters for fraud detection. As fraud tactics evolve with time, having flexible software enables insurers to effectively combat the ever-changing schemes.

III. Continuous Modernization of Processes

Insurance businesses have had to adapt to change over the past few years, and to an extent, their tech investments have played a crucial role in making this happen. The best claims software is one that future-proofs businesses and evolves with changing business needs, customer expectations, and technological innovations. Cloud-based claims management software helps insurers avoid the risk of being tethered to outdated technology while ensuring that the system remains current and adaptable to future needs and innovations.

IV. Enhance Collaboration Across Teams

Claims management often involves multiple departments, such as underwriting, customer service, and legal. Claims software facilitates cross-team communication by offering centralized data access and real-time updates. This fosters collaboration, eliminates silos, and speeds up claims resolution, improving both efficiency and customer satisfaction.

V. Better Planning with Predictive Analytics

Claims management solutions equipped with data analytics help forecast trends like claims volume, settlement time, and fraud risks. Insurers use these insights to allocate resources more effectively, prepare for potential surges, and refine their strategies. Proactive planning enabled by analytics reduces downtime and ensures a more efficient claims process.

What Is the Future of Claims Management?

The future of claims management is increasingly shaped by automation, artificial intelligence, and real-time data processing. Insurers are moving toward intelligent claims ecosystems where AI can assess damages, detect fraud, and approve straightforward claims within minutes. Technologies like computer vision and predictive analytics are reducing human dependency while enhancing accuracy. This shift allows insurers to deliver faster, more transparent claims experiences, which are becoming critical in customer retention and competitive differentiation.

Going forward, claims management will evolve into a proactive, customer-centric function rather than a reactive process. Integration with IoT devices, telematics, and connected ecosystems will enable real-time claims reporting and prevention. Insurers will focus on personalized communication, digital self-service, and seamless omnichannel experiences. Additionally, advanced analytics will continuously optimize decision-making, ensuring improved loss ratios, operational efficiency, and regulatory compliance in a rapidly changing insurance landscape.

Final Words

Claims management software transforms profit margins by eliminating hidden costs, fixing value leaks, and delivering architectural advantages traditional methods can’t match. The hidden costs discussed, value bleeding identified, software benefits outlined, and ROI guidance provided show that modern claims systems directly improve profitability.

Insurers adopting claims software will improve margins measurably, while those avoiding modernization will continue bleeding value through inefficiencies that compound over time.

Case in Focus

An independent insurer struggled with the absence of an insight-based decision-making system, which contributed to the underutilization of data and poor decision-making. The client leveraged our Build-Your-Team (BYT) model to create a powerful business intelligence (BI) tool. The integrated BI platform helped the insurer achieve impressive results, such as a 50% reduction in development costs and improved claims fraud detection. For more details, refer to the complete case study.

Frequently Asked Questions

Claims management software enhances accuracy by embedding business rules, coverage logic, and decision thresholds directly into workflows. This ensures adjusters follow consistent evaluation criteria across claims, reducing subjective judgment errors and maintaining uniform interpretation of policy terms, even as claim volumes and complexity increase.

AI plays a decision-augmentation role in modern claims software, assisting with triage, severity prediction, fraud detection, and settlement recommendations. It accelerates decision-making while maintaining human oversight, enabling insurers to apply intelligence early in the claims lifecycle where it has the greatest financial and customer impact.

The software embeds decision logic early in the claims lifecycle, enabling faster severity assessment and adjudication. Automated workflows and system-driven alerts prevent claims from stalling, significantly reducing end-to-end processing time compared to traditional, manual approaches.

Claims management software uses analytics and AI to detect anomalous patterns across claims, claimant behavior, and historical data. Suspicious claims are flagged early for investigation, reducing fraudulent payouts while allowing legitimate claims to be processed quickly and without disruption.